The Social Security Financing Bill (PLFSS) 2026, presented against a backdrop of budgetary constraints and the quest for efficiency in the social system, includes a number of measures impacting on payroll and payroll management.

Here are the key developments to anticipate now.

The employer contribution increased to 40% for contractual terminations and retirements

The employer's contribution on indemnities paid in the event of individual contractual termination or retirement would increase from 30% to 40%.

Impacts Increase in the cost of negotiated departures and workforce management plans.

Elimination of the exemption from payroll taxes on apprentices' wages

Exemption from employee contributions on the remuneration of apprentices up to 50% of the SMIC would be completely deleted except for CSG/CRDS from January 1, 2026.

Impact reduction in net income for apprentices.

Increase in the social security contribution base to 8%

FS 8% will now include :

- the employer's contribution to the financing of meal vouchers,

- CESU,

- vacation vouchers (for their tax-exempt portion),

- personal assistance,

- financing sports facilities,

- contributions from employers to finance social and cultural activities or services (gifts and vouchers, although it is not clear whether this will apply to those granted by the CSE).

Impacts Increase in the cost of employee benefit policies and the CSE budget.

Creation of additional birth leave

It would be 1 or 2 months for the father or mother, possibly both at the same time, to be taken :

- following maternity leave

- and/or paternity leave.

Impact : business continuity, replacement planning.

JEI: Further increase in the «research expenditure» criterion»

The «research expenditure» criterion would increase from 20% to 25%. Consequently, for JECs, the range for this criterion would be 5% to 25%.

Impact: potential loss of eligibility in the event of a reduction in R&D investment.

Physician-prescribed sick leave capped

The PLFSS provides for :

A cap at 15 days (city) or 30 days (hospital) for initial stops,

An overall cap of 3 years IJSS sickness benefits,

AT/MP: capping at 4 years of IJSS for the same condition. Beyond that: the will be transferred to the employer.

Impact : probable decrease in sick leave

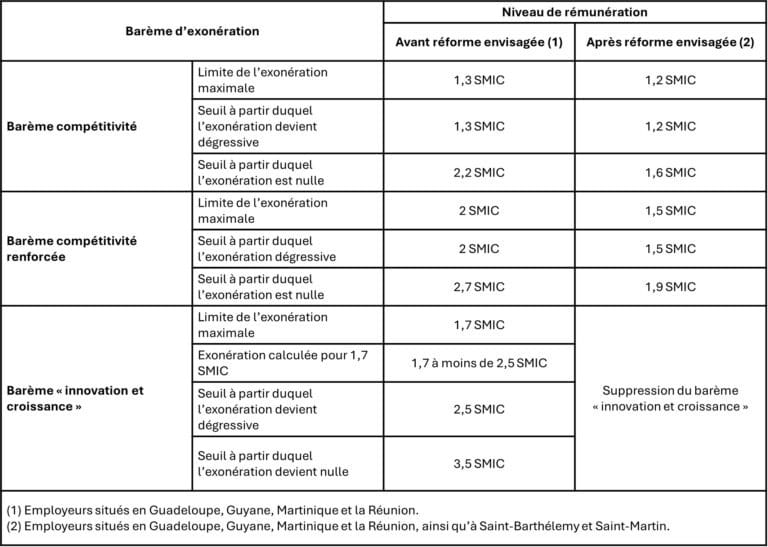

Reduction in LODEOM exemptions